Should I Hire a Tax Professional For My Small Business?

Do I really need a tax professional?

For taxpayers with the simplest income tax returns, do-it-yourself software and websites often seem like the way to go. These individuals often have only one source of income (i.e. W2 from their employer), may have a home mortgage with interest, some student loan debt and maybe some childcare credits. But for those with more complex situations, such as revenue from businesses, income from interest and dividends, capital gains on a home sale or foreign assets, seeking the expertise of a professional can save time, money and potential legal complications.

For small business owners, and many other taxpayers, there are several reasons why seeking a tax professional might be better than going it alone. In this post, we’ll discuss some of the most common and influential drivers that typically signal it’s time to make the switch.

Types of Tax Advisors

The first thing to know is that anyone can claim to be a tax expert. Furthermore, there is no requirement that people who prepare tax returns have to be licensed by the IRS. With that being said, note that there are (generally) three designations when it comes to tax professionals:

- Enrolled agent (EA). An EA is licensed by the IRS and has either passed a difficult test or has at least five years of experience working for the IRS. EAs are “generally” the least expensive of the tax pros and often offer bookkeeping and accounting assistance.

- Certified public accountant (CPA) and other accountants. CPAs are licensed and regulated by each state. They perform sophisticated accounting and business-related tax work and prepare tax returns. Larger businesses or businesses with complex business tax returns often use CPAs. The larger CPA firms (e.g. The Big 4) are expensive. Smaller CPA firms and practitioners can be less expensive and may be better suited for the typical small business.

- Tax Attorneys. Tax Attorneys are lawyers with a special tax law degree (called an L.L.M. in taxation) or a tax specialization certification from a state bar association. Tax attorneys can be expensive, but you should consult one if you have a tax problem, are in criminal trouble with the IRS, need legal representation in court, or need business and estate planning.

Reasons to Hire A Tax Professional

So when is the right time to hire one of the individuals listed above? Typically, it’s once one of the following items below occurs:

- Your tax situation exceeds your expertise or your software. Even what may seem like a “straightforward” situation can quickly turn into more than one bargained for. For example, let’s say that you drive for one of those ride share companies. At tax time, you receive a Form 1099-K, a Form 1099-MISC and a Yearly Summary. Some of the documents include numbers from one of the other documents, and some documents appear to have totally different numbers. Some have fees that “may be deductible” but you aren’t sure which ones to include. Do you add them all? Do you only include some? What if you leave a number off that should have been reported? A tax professional can help ensure everything is reported correctly and that you don’t wind up getting an IRS Automated Adjustment Notice for under reporting your income.

- Your time is valuable and you’re spending too much of it preparing your return. While you may be able to prepare your taxes yourself for $100 or less online, many do-it-yourself filers spend an enormous amount of time when doing so. According to the 2018 Form 1040 Instructions per the IRS, the average taxpayer will spend 11 hours preparing their return.

This number jumps to 19 hours if you have a business! Hiring a professional can reduce that to the time it takes to gather your tax documents and forward them to their office, go over a few items with them and then review the final return for accuracy. If your time is better spent closing sales deals, running your business or spending it with family and friends, then hiring a tax professional can make perfect cents (pun intended).Average Taxpayer Burden for Individuals Average Time (Hours) Type of Taxpayer Percentage

of ReturnsTotal

TimeRecord

Keeping

Tax

Planning

Form

Completion &

SubmissionAll

Other

Average

Cost

(Dollars)All taxpayers 100% 11 5 2 4 1 $200 Nonbusiness 70% 7 2 1 3 1 $110 Business 30% 19 10 3 5 1 $400 Estimated Average Taxpayer Burden for Individuals by Activity per 2018 Form 1040 Instructions - You could be missing out on valuable deductions. In addition to saving you countless hours of painfully boring and costly tax guessing, experienced preparers know the deductions that you may qualify for, and which items are tax deductible if you own a business. They can also easily tell you if it’s more beneficial to itemize or take the standard deduction. Even if you just earn only a little income on the side, a professional may be able to find you deductions or credits that will more than pay for their services and keep more of your hard earned money out of the pockets of Uncle Sam. Lastly, the cost of having your taxes prepared by a professional can also be tax deductible as a professional fee if you have a business.

- The tax law is constantly changing. Adding to the complexity, new tax laws are enacted every year that affect virtually everyone, making it tough to keep up with changes and how they might affect you. For example, the new 20% Qualified Business Income Deduction will no doubt cause some frustration for those this tax year (especially if you in the “phase in” range for a partial deduction). For small businesses that have to manage income tax withholding and reporting for their employees, taxes are even more complex. While tax software can help, an experienced professional that “has seen it all before,” and also keeps up with tax law changes through educational courses, can make the process easy peasy lemon squeezy!

- A mistake was made in the past. If you do your taxes yourself, you are much more likely to make a mistake. Mistakes happen, but when they happen to you, it may feel like they are costing you big time. A simple math error can cause a return to be inaccurate, leaving you liable for unpaid taxes and interest. For errors the IRS believes are not accidental, such as failing to report income, taxpayers can also face large fines and even criminal prosecution. A skilled tax professional can not only help ensure that your returns are accurately prepared, but they often can help you rectify a past mistake.

- You want peace of mind. The only people that look forward to an IRS audit are IRS auditors! The best way to avoid their scrutiny is to make sure your tax return is in compliance with the tax laws. To do that, why not hire a professional who lives, works and breathes taxes every day (or at least a lot more frequently than you do)? There is still a chance than any taxpayer will get audited, but if you use the services of a professional CPA, Enrolled Agent or Tax Attorney, and your return is selected for further inspection by the IRS, those professionals can typically help represent you on your behalf before the IRS. Don’t go before a court without a lawyer, and don’t go before the IRS without a professional.

How much does it cost to hire a tax professional?

According to the 2018 survey by the National Society of Accountants, the average federal tax return in the U.S., including the tax return for the person’s state of residence, cost $294 for a professional preparer to handle if the taxpayer itemizes and $188 if they don’t. If you own a business that needs to file a Schedule C (for business income and expenses) that will tack on $187 more. But as outlined above, there are numerous reasons why this cost can be well worth it.

Do you need help with your business taxes this year?

If you don’t want to deal with the hassle and headache of navigating the new tax law, or simply don’t have the time, we’d be happy to assist you! Call the office now to schedule your appointment or request your complementary tax situation analysis (valued at $197 but free if you mention this blog post). We are a year round practice and can even help you file your state taxes no matter where you are located.

What is the 20% QBI Deduction?

In late 2017 with the passage of the Tax Cuts and Jobs Act (TCJA), a new 20% deduction for pass through businesses was created. This deduction is also known as the section 199A deduction, the deduction for qualified business income (QBI), the 20% deduction and the pass-through deduction. In this post, we’ll discuss who can take the deduction, how it is calculated and provide some examples to aid in ones understanding.

Who may take the section 199A deduction? Generally speaking, individuals, trusts and estates with QBI, qualified REIT dividends or qualified publicly traded partnership (PTP) income may qualify for the deduction. This income must be derived from a qualified trade or business operated directly or through a pass-through entity. From an “entity” standpoint, the following are those that may be able to take the deduction:

- Partnerships

- S-Corporations

- Sole proprietorship’s (i.e. Schedule C filers)

- LLCs

- Real estate investors

- Trusts, estates, REITs and qualified cooperatives

So as you can see, the deduction is intended for those entities that are not classified as C-Corporations. Why? We’ll since the TCJA cut the corporate income tax rate to a flat 21%, this was the way to replicate a similar treatment for those entities that were not structured as such.

What is QBI? QBI is the net amount of qualified income, gain, deduction and loss from any qualified trade or business. Only items included in taxable income are counted. In addition, the items must be effectively connected with a U.S. trade or business. Items such as capital gains and losses, certain dividends and interest income are excluded.

What is not QBI? QBI is not items used in determining net long-term capital gain or loss, dividends, interest income, reasonable compensation, guaranteed payments or amount paid or incurred by a partnership to a partner who is acting other than in his or her capacity as a partner for services

What is a qualified trade or business? It is any trade or business other than one of the following:

- One that is defined as a specified service trade or business (SSTB), which includes those that involve the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading, dealing in certain assets or any trade or business where the principal asset is the reputation or skill of one or more of its employees.

- One that involved performing services as an employee (i.e. one in which you receive a W2)

What information should my K1 have on it for me to take the QBI deduction? If a K1 fails to report any item below, the IRS will presume that the QBI, W-2 wages and the unadjusted basis immediately after acquisition (UBIA) of qualified property are equal to zero:

- Whether the business is an SSTB.

- Whether there is more than one trade or business.

- QBI for each trade or business.

- W-2 wages and UBIA of qualified property.

- Any REIT dividends.

- Any PTP income.

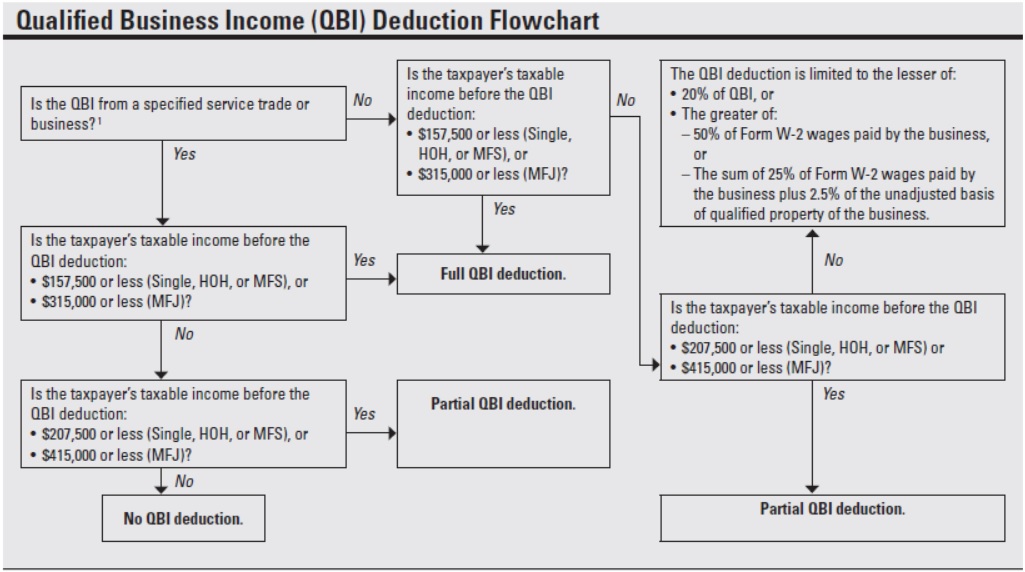

How is the deduction for QBI calculated? Now this is where things “can” get complicated. In the simplest application, the deduction is equal to 20% of domestic QBI from a qualified trade or business. The deduction is taken on an individuals personal return and “below the line.” Thus, it reduces taxable income and not adjusted gross income (AGI). The following 199A Calculator will give you a quick idea of how it works and what a QBI deduction might look like for your situation.

The calculation itself, is dependent on the taxable income reflected on the taxpayers return:

Below threshold: If a taxpayer’s taxable income is below $315,000 for a married couple filing a joint return and $157,500 for all other taxpayers; the deduction is the lesser of:

- 20% of the taxpayer’s QBI, plus 20 percent of the taxpayer’s qualified real estate investment trust (REIT) dividends and qualified PTP income or

- 20% percent of the taxpayer’s taxable income minus net capital gains.

So basically, the deduction will never be greater than 20% of the taxpayers QBI or their taxable income. Now what happens if the income is above the amounts specified above?

Between threshold: If the taxpayer’s taxable income is between thresholds (i.e., between $315,000 and $415,000 for married taxpayers filing jointly; between $157,500 and $207,500 for others), the QBI deductible amount for the business is subject to a limitation based on W-2 wages and/or UBIA. In these instances, the deduction is calculated as:

- 20% of QBI for that trade or business less,

- An amount equal to the reduction ratio multiplied by the excess amount.

- The “reduction ratio” is calculated as (Taxable income – $315,000)/$100,000 for those filing MFJ and (Taxable income – $157,500)/$50,000 for all other taxpayers

- The “excess amount” is the amount by which 20% of QBI exceeds the greater of:

- 50% of Form W-2 wages paid by the business, or

- 25% of Form W-2 wages paid by the business plus 2.5% of the UBIA

Above threshold: If the taxpayer’s taxable income is above the thresholds (i.e., $415,000 for married taxpayers filing jointly and $207,500 for others), the deduction is:

- the lesser of

- 20% of QBI for that trade or business OR

- the greater of

- 50% of W-2 wages for that trade or business OR

- 25% of W-2 wages for that trade or business PLUS 2.5% of the UBIA of all qualified property

I have income from a SSTB. How does that affect my deduction? Your ability to take the deduction will depend on your taxable income and will be calculated as follows:

- The limitation does not apply to any taxpayer whose taxable income is below the $315,000/$157,500 threshold amounts.

- For taxpayers whose taxable income is within the phase-in range ($315,000 to $415,000 for joint filers and $157,500 to $207,500 for all other filing statuses), the taxpayer’s share of QBI, W-2 wages and UBIA of qualified property related to the SSTB may be limited/reduced (see Example 5 below)

- If the taxpayer’s taxable income exceeds the phase-in range (i.e. greater than $415,000 for joint filers and $207,500 for all other filing statuses), no deduction is allowed with respect to any SSTB.

I am a visual person. Do you have a flowchat to illustrate what all of the above means?

Ask and you shall receive. Take a look at the graphic below (absent some of the calculations).

Calculation examples using various ranges and business types. On August 8, 2018, the IRS released proposed regulations on §199A, providing guidance on their interpretation of provisions regarding the new 20% deduction for pass-through entities. The proposed regulations span 184 pages and provide numerous definitions, examples, and anti-abuse provisions. As such, it’s a good idea to review the examples in the link (see page 114/184) as the IRS has outlined computations for many scenarios.

The examples shown below are designed to help you gain a general understanding of how the information presented above comes into play.

Income below threshold examples

Example 1 In 2018, Pilar, an unmarried individual, operated an accounting and tax business (a SSTB) as a sole proprietor and earned a net Schedule C income of $100,000. She did not have any capital gains or losses. She claimed the standard deduction of $12,000 so her taxable income was equal to $88,000.

Pilar’s QBI deduction is $17,600, the lesser of 20% of her QBI ($100,000 x 20% = $20,000) or her taxable income minus long-term capital gain ($88,000 x 20% = $17,600). Because she is in the lowest range, the fact that she operates SSTB is irrelevant.

Example 2 Assume the same facts as above except that Pilar had $7,000 in long term capital gains. Pilar’s QBI deduction is $16,200, the lesser of 20% of her QBI ($100,000 x 20% = $20,000) or her taxable income minus long-term capital gain ($88,000 – 7,000 = $81,000 x 20% = $16,200).

Example 3 Popeye and Olive Oyl are married and file a joint individual income tax return. Popeye earned $300,000 in wages as an employee for the Department of Defense in 2018. Olive Oyl owns 100% of the shares of Alessi, an S corporation that manufactures olive oil. Alessi generated $100,000 in net income from operations in 2018. Alessi paid Olive Oyl $150,000 in wages in 2018. Neither Popeye or Olive Oyl have any capital gains or losses. After allowable deductions not related to Alessi (i.e. personal itemized deductions) , Popeye and Olive Oyl’s total taxable income for 2018 is $300,000.

Popeye and Olive Oyl’s wages are not considered to be income from a trade or business for purposes of the QBI deduction. Because Alessi is an S corporation, its QBI is determined at the S corporation level. Alessi’s QBI is $100,000, the net amount of its qualified items of income, gain, deduction, and loss. The wages paid by Alessi to Olive Oyl are considered to be a qualified

item of deduction for purposes of determining Alessi’s QBI.

The QBI deduction with respect to Alessi’s QBI is then determined by Olive Oyl, Alessi’s sole shareholder, and is claimed on the joint return filed by Popeye and Olive Oyl. Their QBI deduction is equal to $20,000, the lesser of 20% of Olive Oyl’s QBI from the business ($100,000 x 20% = $20,000) or 20% of Popeye and Olive Oyl’s total taxable income for the year ($300,000 x 20% = $60,000).

Income within threshold examples

These limitations are phased in for joint filers with taxable income between $315,000 and $415,000, and all other taxpayers with taxable income between $157,500 and $207,500.

Example 4 Bonnie and Clyde are married and file a joint individual income tax return. Bonnie is a shareholder in Public Enemy, an entity taxed as an S corporation for Federal income tax

purposes that conducts a single trade or business (freight operations). Public Enemy holds no qualified property.

Bonnie’s share of Public Enemy’s QBI is $300,000 in 2018. Bonnie’s share of the W-2 wages from Public Enemy in 2018 is $40,000. Clyde earns wage income from employment by an unrelated company. After allowable deductions unrelated to Public Enemy, Bonnie and Clyde’s taxable income for 2018 is $375,000. Bonnie and Clyde are within the phase-in range because their taxable income exceeds the applicable threshold amount, $315,000, but does not exceed the threshold, or $415,000. Consequently, the QBI component of Bonnie and Clyde’s QBI deduction may be limited by the W-2 wage and UBIA limitations but the limitations will be phased in.

The UBIA of qualified property limitation amount is zero because Public Enemy does not hold

qualified property. Bonnie and Clyde must apply the W-2 wage limitation by first determining

20% of Bonnie’s share of Public Enemy’s QBI. This amount equals $60,000 ($300,000 x 20%). Next, Bonnie and Clyde must determine 50% of Bonnie’s share of Public Enemy ’s W-2 wages. This amount is $20,000 ($40,000 x 50%).

Because 50% of Bonnie’s share of Public Enemy’s W-2 wages ($20,000) is less than 20% of her share of Public Enemy’s QBI ($60,000), Bonnie and Clyde must determine the QBI component of deduction by reducing 20% of Bonnie’s share of Public Enemy’s QBI by the reduction amount.

Bonnie and Clyde are 60% through the phase-in range (that is, their taxable income of $375,000 exceeds the threshold amount by $60,000 and their phase-in range is $100,000). Bonnie and Clyde must determine the excess amount, which is the excess of 20% of Bonnie’s share of Public Enemy’s QBI, or $60,000, over 50% of Bonnie’s share of Public Enemy’s W-2 wages, or $20,000. Thus, the excess amount is $40,000. The reduction amount is equal to 60% of the excess amount, or $24,000 ($40,000 x 60%).

Thus, the QBI component of Bonnie and Clyde’s deduction is equal to $36,000, 20% of Bonnie’s $300,000 share Public Enemy’s QBI (that is, $60,000), reduced by $24,000. Bonnie and Clyde’s QBI deduction is equal to the lesser of (i) 20% of the QBI from the business as limited ($36,000) or (ii) 20% of Bonnie and Clyde’s taxable income ($375,000 x 20% = $75,000). Therefore, Bonnie and Clyde’s deduction is $36,000 for 2018.

Example 5 Assume the same facts as in Example 4, except that Public Enemy was engaged in a SSTB (consulting). Because Bonnie and Clyde are within the phase-in range, Bonnie must reduce the QBI and W-2 wages allocable to Bonnie from Public Enemy to the applicable percentage of those items as a proportion to the phase out range. Furthermore, she must apply a reduction amount to the calculation.

The applicable percentage equals 100% minus the percentage obtained by dividing (a) the pre-QBI deduction taxable income of the taxpayer in excess of the applicable threshold amount by (b) $100,000 for joint-return filers or $50,000 for other filers. Reduction amount means, the excess amount multiplied by the applicable percentage. It is calculated as 20 percent of QBI over the greater of 50 percent of W-2 wages or the sum of 25 percent of W-2 wages plus 2.5 percent of the UBIA of qualified property.

For Bonnie and Clyde’s applicable percentage, their taxable income ($375,000) exceeds their threshold amount ($315,000) by $60,000. A ratio of 60% (i.e. $60,000/$100,000) is what is used to find their applicable percentage of 40% (i.e. 100% – 60% = 40%). Accordingly, in computing the QBI deduction, the couple would only be allowed to take into account 40% of the QBI, W-2 wages, and qualified property with respect to the trade or business.

Thus Bonnie’s QBI is “adjusted” to $120,000 ($300,000 x 40%) and her share of W-2 wages is “adjusted” to $16,000 ($40,000 x 40%). These “adjusted” numbers must then be used to determine how Bonnie’s QBI deduction is limited. The deduction will be limited to the lesser of:

- (i) 20% of Bonnie’s share of Public Enemy’s QBI or

- (ii) the greater of the W-2 wage or UBIA of qualified property limitations.

- Twenty percent of Bonnie’s share of QBI of $120,000 is $24,000.

- The W-2 wage limitation equals 50% of Bonnie’s share of Public Enemy’s wages ($16,000 x 50%) or $8,000.

- The UBIA of qualified property limitation equals $0

To calculate the reduction amount Bonnie and Clyde must first determine the excess amount. This is calculated as the excess of 20% of Bonnie’s share of Public Enemy’s QBI, as adjusted ($24,000), over 50% of Bonnie’s share of Public Enemy’s W-2 wages, as adjusted ($8,000). Thus, the excess amount is $16,000. The reduction amount is equal to 60% of the excess amount or $9,600. Thus, the QBI component of Bonnie and Clyde’s QBI deduction is equal to $14,400 ($24,000 – $9,600).

As Bonnie and Clyde’s QBI deduction is equal to the lesser of (i) 20% of the QBI from the business as limited ($14,400) or 20% of Bonnie’s and Clyde’s taxable income ($375,000 x 20% = $75,000), their QBI deduction is $14,400 for 2018.

Income above threshold examples

Example 6 Ernie, an unmarried individual, is a 30% owner of Bert LLC, which is classified as a partnership for Federal income tax purposes. In 2018, Bert LLC has a single trade or business (landscaping) and reported QBI of $3,000,000. Bert LLC paid total W-2 wages of $1,000,000, and its total UBIA of qualified property is $100,000. Ernie is allocated 30% of all items of the partnership. For the 2018 taxable year, Ernie reports $900,000 of QBI ($3,000,000 x 30%) from Bert LLC . After allowable deductions unrelated to Bert LLC (i.e. personal itemized deductions), Ernie’s taxable income is $880,000.

Because Ernie’s taxable income is above the threshold amount, the QBI component of Ernie’s QBI deduction will be limited to the lesser of:

- (i) 20% of Ernie’s share of Bert LLC’s QBI or

- (ii) the greater of the W-2 wage or UBIA of qualified property limitations.

So while it might not be clear, there are three calculations related to the two bullets above:

- Twenty percent of Ernie’s share of QBI of $900,000 is $180,000.

- The W-2 wage limitation equals 50% of Ernie’s share of Bert LLC’s wages ($1,000,000 x 30% = $300,000 x 50%) or $150,000.

- The UBIA of qualified property limitation equals $75,750, the sum of:

- (i) 25% of Ernie’s share of Bert LLC’s wages ($1,000,000 x 30% = $300,000 x 25%) or $75,000 plus

- (ii) 2.5% of Ernie’s share of UBIA of qualified property ($100,000 x 30% = $30,000 x 2.5%) or $750.

For items 2 and 3 above, the greater of the limitation amounts ($150,000 and $75,750) is $150,000.

The QBI component of Ernie’s QBI deduction is thus limited to $150,000, the lesser of (i) 20% of QBI ($180,000) and (ii) the greater of the limitations amounts ($150,000). Ernie’s QBI deduction is equal to the lesser of (i) 20% of the QBI from the business as limited ($150,000) or (ii) 20% of Ernie’s taxable income ($880,000 x 20% = $176,000). Therefore, Ernie’s QBI deduction is $150,000 for 2018.

Ready to get help? As you can tell, the computations involved in taking the deduction get more complicated depending on the taxpayers income. If you don’t want to go through the mechanics of calculating your QBID and ensuring it is correct, why not let a professional do the work? Feel free to give us a call or drop us an email and we’d be happy to assist you ensure that everything is done correctly. Plus, you won’t have to spend the time doing it!

What Is An Eligible Education Institution?

Do I get a tax write off for this?

The IRS provides taxpayers certain tax breaks when you pay for education. However, there is a catch. The monies paid (i.e. tuition) have to be to an eligible education institution. What exactly is that? Read on my friend.

Tax Benefits Available

The following are the benefits commonly available to taxpayers:

- Tuition and Fees Deduction: The tuition and fees deduction can reduce the amount of your income subject to tax by up to $4,000. You may be able to deduct qualified education expenses for higher education paid during the year for yourself, your spouse or your dependent.

- American Opportunity Tax Credit: A credit for tuition, required enrollment fees and course material for the first four years of post-secondary education for up to $2,500 per eligible student per year. Your modified adjusted gross income (MAGI) must be under $90,000 ($180,000 for joint filers) and you must not have claimed the AOTC or the former Hope Credit for more than four tax years for the same eligible student. Forty percent of this credit may be refundable.

- Lifetime Learning Credit: The Lifetime Learning Credit is 20% of the first $10,000 of qualified education expenses paid for all eligible students. The maximum credit is $2,000 per return regardless of the number of eligible students. There is no limit on the number of years the credit can be claimed for each student; thus the reason it is referred to as “lifetime.”

Eligible Education Institution Defined

An eligible educational institution is a school offering higher education beyond high school. It is any college, university, trade school, or other post secondary educational institution eligible to participate in a student aid program run by the U.S. Department of Education. This includes most accredited public, nonprofit and privately-owned–for-profit post secondary institutions.

With that said, if you are attending a school in another country, there is a possibility that it is NOT considered an eligible education institution. In general, if you aren’t sure if your school is an eligible educational institution:

• Ask your school (i.e. someone in the financial aid department) if it is, or

• See if your school is on the U.S. Federal Student Aid Code List.

TIP: A small number of schools, not on the list, may be eligible educational institutions and the school can confirm that for you.

IRS “Expanded” Installment Agreement

Complete this form to set up your IRS payment plan!

When a person owes the IRS money that they can’t pay in full, they typically will qualify to deal with the debt via a payment plan. This payment plan is called an “installment agreement” in IRS terminology. Simply stated, an installment agreement is a contract with the IRS to pay the taxes you owe within an extended time frame. There are many types of installment agreements, but two of the most common are the guaranteed and streamlined variety.

Guaranteed & Streamlined Installment Agreements

We discuss the guaranteed installment agreement at length in this blog post. But what exactly is a streamlined installment agreement? For individual taxpayers who have filed all required returns and have an assessed balance of tax, penalties and interest of $50,000 or less, they can enter into an installment agreement with “relaxed” criteria. Basically, they don’t have to go through as many hoops or submit as much documentation. The following criteria apply to those who wish to apply for a streamlined installment agreement:

- Payment Terms Up to 72 months – or – the number of months necessary to satisfy the liability in full by the Collection Statute Expiration Date (CSED), whichever is less

- Collection Information Statement (financials) Not required.

- Payment Method Direct debit payments or payroll deduction is preferred, but not required.

- Notice of Federal Tax Lien

- Determination not required for assessed balances up to $25,000.

- Determination is not required for assessed balances of $25,001 – $50,000 with the use of direct debit or payroll deduction agreement. If taxpayer does not agree to direct debit or payroll deduction, then they still qualify for Streamlined IA over $25,000, but a Notice of Federal Tax Lien determination will be made.

The criteria discussed above also apply to business taxpayers, but only for income tax debts up to $25,000.

So what if you owe more than $50,000 as an individual or $25,000 as a business? Well, this is where the “expanded installment agreement” comes into play.

Expanded Installment Agreements

From late 2016 through late Fall of 2018, the IRS tested “expanded” criteria for the streamlined processing of taxpayer requests for installment agreements. During the test, taxpayers who owed more than $50,001 but less than $100,000 were allowed to use most of the criteria outlined under the streamlined installment agreement. Well, based on test results, the expanded criteria for streamlined processing of installment agreement requests were made permanent. If you are a practitioner, you can find the “new” criteria in IRM 5.19.1.6.4 under item “11” (09-26-18 update).

So, for individual taxpayers who have filed all required returns and have an assessed balance of tax, penalties and interest between $50,001 and $100,000, you can use the following criteria to apply for an expanded installment agreement:

- Payment Terms Up to 84 months – or – the number of months necessary to satisfy the liability in full by the Collection Statute Expiration date, whichever is less

- Collection Information Statement (financials) Not required if the taxpayer agrees to make payment by direct debit or payroll deduction

- Payment Method Direct debit payments or payroll deduction is not required; however, if one of these methods is not used, then a Collection Information Statement is required.

- Notice of Federal Tax Lien

- Determination is required.

The criteria discussed above also applies to all out of business sole-proprietorship debts between $50,001 and $100,000.

Do you owe the IRS and need to enter into a resolution option?

Check out this page of our website where you can receive our special report entitled 5 Questions To Ask Any Tax Resolution Firm Before Paying Them A Dime, a comprehensive 30-minute Tax Debt Settlement Analysis AND your personalized Tax Resolution Plan (a package valued at $175, but FREE to you for a limited time). You can also visit this page to read about how you can find out the date (i.e. CSED) the IRS will write off your tax debt!

Can The IRS Revoke My Passport?

Don’t want to pay your taxes ehh? We’ll get your attention!

So the short answer to the question is yes, the IRS can revoke your passport if you have a “seriously delinquent” tax debt. But what exactly does that mean? More importantly, what can you do if your passport is at risk of being revoked? Read on to learn more my friend!

Background

On December 4, 2015, President Obama signed the Fixing America’s Surface Transportation (FAST) Act (Pub. L. No. 114-94) into law—the first federal law in over a decade to provide long-term funding certainty for surface transportation infrastructure planning and investment. But like all legislative bills/acts, other things that may appear unrelated often get inserted into them. This act was no different.

Internal Revenue Code Sec. 7345 was enacted as part of the FAST Act. A seriously delinquent tax debt is defined as an unpaid, legally enforceable, and assessed federal tax liability greater than $51,000 (adjusted annually for inflation) and for which:

- The IRS has filed a notice of federal tax lien and the individual’s right to a hearing has been exhausted or lapsed, or

- The IRS has issued a levy.

Generally speaking a federal tax debt is the sum of all current tax obligations, including penalties and interest. However, a “seriously delinquent tax debt” does not include any of the following tax debt even if it meets the criteria stated above:

- Being paid timely with an IRS-approved installment agreement (IA),

- Being paid timely with an offer in compromise (OIC) accepted by the IRS, or a settlement agreement entered with the Justice Department,

- For which a collection due process hearing is timely requested regarding a levy to collect the debt,

- For which collection has been suspended because a request for innocent spouse relief under IRC § 6015 has been made

Furthermore, a passport won’t be at risk under this program for any taxpayer:

- Who is in bankruptcy

- Who is identified by the IRS as a victim of tax-related identity theft

- Whose account the IRS has determined is currently not collectible (CNC) due to hardship

- Who is located within a federally declared disaster area

- Who has a request pending with the IRS for an installment agreement (IA)

- Who has a pending offer in compromise (OIC) with the IRS

- Who has an IRS accepted adjustment that will satisfy the debt in full

What the IRS does when you have a seriously delinquent tax debt

The IRS is required to notify you in writing at the time the IRS certifies seriously delinquent tax debt to the State Department. This is done via IRS notice CP 508C. If you have been certified to the Department of State by the Secretary of the Treasury as having a seriously delinquent tax debt, you cannot be issued a U.S. passport and your current U.S. passport may be revoked.

How do you resolve the situation?

The IRS will reverse a certification when the tax debt no longer qualifies as a seriously delinquent tax debt. This happens when:

-

- The tax debt is fully satisfied or becomes legally unenforceable.

- The tax debt is no longer seriously delinquent meaning:

- You and the IRS enter into an installment agreement allowing you to pay the debt over time.

- The IRS accepts an offer in compromise to satisfy the debt.

- The Justice Department enters into a settlement agreement to satisfy the debt.

- Collection is suspended because you request innocent spouse relief under IRC § 6015.

- You make a timely request for a collection due process hearing regarding a levy to collect the debt.

- The certification is erroneous.

The IRS will make this reversal within 30 days and provide notification to the State Department as soon as practicable.

The IRS will not reverse certification where a taxpayer requests a collection due process hearing or innocent spouse relief on a debt that is not the basis of the certification. Also, the IRS will not reverse the certification because the taxpayer pays the debt below $50,000. So…if you have been notified that your tax debt has been certified, you should consider:

- paying the tax owed in full,

- entering into an installment agreement, or

- making an offer in compromise.

But what if the IRS made an error?

The State Department is held harmless in these matters and cannot be sued for any erroneous notification or failed decertification under IRC § 7345. If you believe that the IRS certified your debt to the State Department in error, you can file suit in the U.S. Tax Court or a U.S. District Court to have the court determine whether the certification is erroneous or the IRS failed to reverse the certification when it was required to do so. If the court determines the certification is erroneous or should be reversed, it can order the IRS to notify the State Department that the certification was in error.

Can I contact the State Department to find out the status of my passport?

The State Department does not have any information about your seriously delinquent tax debt. For questions, or to resolve your seriously delinquent tax debt, they recommend that you contact the IRS via phone at 1-855-519-4965 (1-267-941-1004 international) of via mail at:

Department of the Treasury

Internal Revenue Service

Attn: Passport

PO Box 8208

Philadelphia, PA 19101-8208

How can we help?

As you can tell from above, the IRS will only really reverse the certification if the debt is no longer enforceable (i.e. collectable) or if you enter into a resolution option (i.e. payment plan, currently not collectible, etc).

With regards to enforceability, the IRS only has 10 years from the date of assessment to collect on unpaid taxes. If you are getting letters, your debt is more than likely still active. But do you know when it will expire? This is called the CSED date.

While you could go through the hassle of calculating your CSED (see this blog post), do you really want to? For a flat fee, and us filing a few forms with the IRS (with your consent), we’ll look at however many years you want to analyze, and provide you with a comprehensive report that will include:

- Total tax assessment, penalty, interest and accrual amounts for each year (so you know how much you really owe)

- CSED calculations for each year requested (i.e. when your debt will expire)

- Tolling events (if any) and the days your CSED has been extended

- All IRS notices sent/received for each year

- IRS account activity by year

- And much, much more (we promise)

If your debt will not expire for some time, we are fully authorized to represent your before the IRS and can can help negotiate a resolution option (i.e. IA, OIC, CNC) that will satisfy the IRS conditions to have your certification revoked/lifted. You can learn more about our representation services by visiting the IRS Debt Representation page or reading the IRS Talk post within our blog.

When you are ready to get started, simply call us at (773) 239-8850 or click our email address at the bottom of this screen.

Click above to watch our Money Management and Tax Chit Chat video series!

Click Above For Your Top Secret Guide To Tax Reduction, Business Success and Solving IRS Debt Problems!

Click Above To Learn 111 Ways To Slash Your Tax Bill!