In late 2017 with the passage of the Tax Cuts and Jobs Act (TCJA), a new 20% deduction for pass through businesses was created. This deduction is also known as the section 199A deduction, the deduction for qualified business income (QBI), the 20% deduction and the pass-through deduction. In this post, we’ll discuss who can take the deduction, how it is calculated and provide some examples to aid in ones understanding.

Who may take the section 199A deduction? Generally speaking, individuals, trusts and estates with QBI, qualified REIT dividends or qualified publicly traded partnership (PTP) income may qualify for the deduction. This income must be derived from a qualified trade or business operated directly or through a pass-through entity. From an “entity” standpoint, the following are those that may be able to take the deduction:

- Partnerships

- S-Corporations

- Sole proprietorship’s (i.e. Schedule C filers)

- LLCs

- Real estate investors

- Trusts, estates, REITs and qualified cooperatives

So as you can see, the deduction is intended for those entities that are not classified as C-Corporations. Why? We’ll since the TCJA cut the corporate income tax rate to a flat 21%, this was the way to replicate a similar treatment for those entities that were not structured as such.

What is QBI? QBI is the net amount of qualified income, gain, deduction and loss from any qualified trade or business. Only items included in taxable income are counted. In addition, the items must be effectively connected with a U.S. trade or business. Items such as capital gains and losses, certain dividends and interest income are excluded.

What is not QBI? QBI is not items used in determining net long-term capital gain or loss, dividends, interest income, reasonable compensation, guaranteed payments or amount paid or incurred by a partnership to a partner who is acting other than in his or her capacity as a partner for services

What is a qualified trade or business? It is any trade or business other than one of the following:

- One that is defined as a specified service trade or business (SSTB), which includes those that involve the performance of services in the fields of health, law, accounting, actuarial science, performing arts, consulting, athletics, financial services, investing and investment management, trading, dealing in certain assets or any trade or business where the principal asset is the reputation or skill of one or more of its employees.

- One that involved performing services as an employee (i.e. one in which you receive a W2)

What information should my K1 have on it for me to take the QBI deduction? If a K1 fails to report any item below, the IRS will presume that the QBI, W-2 wages and the unadjusted basis immediately after acquisition (UBIA) of qualified property are equal to zero:

- Whether the business is an SSTB.

- Whether there is more than one trade or business.

- QBI for each trade or business.

- W-2 wages and UBIA of qualified property.

- Any REIT dividends.

- Any PTP income.

How is the deduction for QBI calculated? Now this is where things “can” get complicated. In the simplest application, the deduction is equal to 20% of domestic QBI from a qualified trade or business. The deduction is taken on an individuals personal return and “below the line.” Thus, it reduces taxable income and not adjusted gross income (AGI). The following 199A Calculator will give you a quick idea of how it works and what a QBI deduction might look like for your situation.

The calculation itself, is dependent on the taxable income reflected on the taxpayers return:

Below threshold: If a taxpayer’s taxable income is below $315,000 for a married couple filing a joint return and $157,500 for all other taxpayers; the deduction is the lesser of:

- 20% of the taxpayer’s QBI, plus 20 percent of the taxpayer’s qualified real estate investment trust (REIT) dividends and qualified PTP income or

- 20% percent of the taxpayer’s taxable income minus net capital gains.

So basically, the deduction will never be greater than 20% of the taxpayers QBI or their taxable income. Now what happens if the income is above the amounts specified above?

Between threshold: If the taxpayer’s taxable income is between thresholds (i.e., between $315,000 and $415,000 for married taxpayers filing jointly; between $157,500 and $207,500 for others), the QBI deductible amount for the business is subject to a limitation based on W-2 wages and/or UBIA. In these instances, the deduction is calculated as:

- 20% of QBI for that trade or business less,

- An amount equal to the reduction ratio multiplied by the excess amount.

- The “reduction ratio” is calculated as (Taxable income – $315,000)/$100,000 for those filing MFJ and (Taxable income – $157,500)/$50,000 for all other taxpayers

- The “excess amount” is the amount by which 20% of QBI exceeds the greater of:

- 50% of Form W-2 wages paid by the business, or

- 25% of Form W-2 wages paid by the business plus 2.5% of the UBIA

Above threshold: If the taxpayer’s taxable income is above the thresholds (i.e., $415,000 for married taxpayers filing jointly and $207,500 for others), the deduction is:

- the lesser of

- 20% of QBI for that trade or business OR

- the greater of

- 50% of W-2 wages for that trade or business OR

- 25% of W-2 wages for that trade or business PLUS 2.5% of the UBIA of all qualified property

I have income from a SSTB. How does that affect my deduction? Your ability to take the deduction will depend on your taxable income and will be calculated as follows:

- The limitation does not apply to any taxpayer whose taxable income is below the $315,000/$157,500 threshold amounts.

- For taxpayers whose taxable income is within the phase-in range ($315,000 to $415,000 for joint filers and $157,500 to $207,500 for all other filing statuses), the taxpayer’s share of QBI, W-2 wages and UBIA of qualified property related to the SSTB may be limited/reduced (see Example 5 below)

- If the taxpayer’s taxable income exceeds the phase-in range (i.e. greater than $415,000 for joint filers and $207,500 for all other filing statuses), no deduction is allowed with respect to any SSTB.

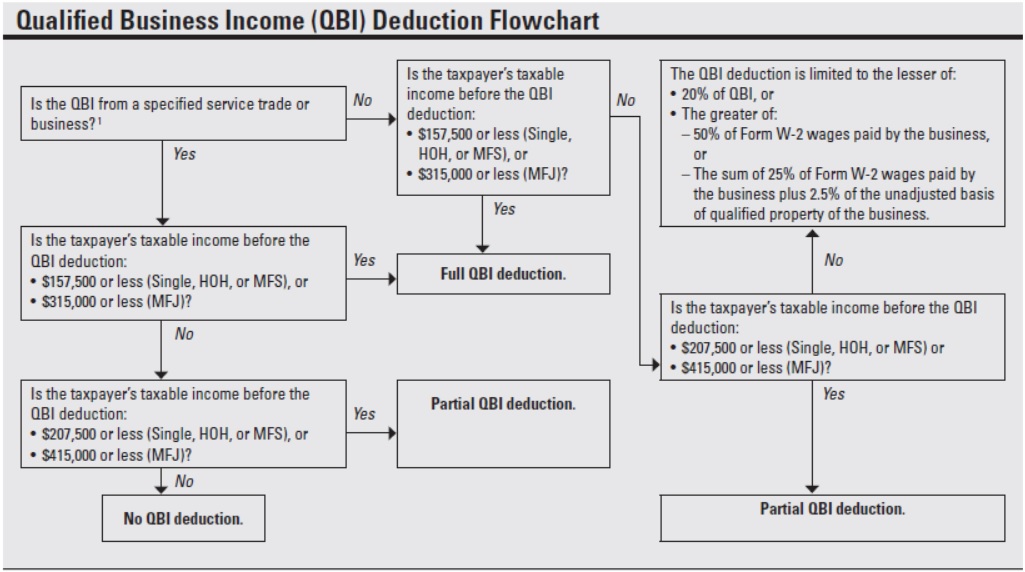

I am a visual person. Do you have a flowchat to illustrate what all of the above means?

Ask and you shall receive. Take a look at the graphic below (absent some of the calculations).

Calculation examples using various ranges and business types. On August 8, 2018, the IRS released proposed regulations on §199A, providing guidance on their interpretation of provisions regarding the new 20% deduction for pass-through entities. The proposed regulations span 184 pages and provide numerous definitions, examples, and anti-abuse provisions. As such, it’s a good idea to review the examples in the link (see page 114/184) as the IRS has outlined computations for many scenarios.

The examples shown below are designed to help you gain a general understanding of how the information presented above comes into play.

Income below threshold examples

Example 1 In 2018, Pilar, an unmarried individual, operated an accounting and tax business (a SSTB) as a sole proprietor and earned a net Schedule C income of $100,000. She did not have any capital gains or losses. She claimed the standard deduction of $12,000 so her taxable income was equal to $88,000.

Pilar’s QBI deduction is $17,600, the lesser of 20% of her QBI ($100,000 x 20% = $20,000) or her taxable income minus long-term capital gain ($88,000 x 20% = $17,600). Because she is in the lowest range, the fact that she operates SSTB is irrelevant.

Example 2 Assume the same facts as above except that Pilar had $7,000 in long term capital gains. Pilar’s QBI deduction is $16,200, the lesser of 20% of her QBI ($100,000 x 20% = $20,000) or her taxable income minus long-term capital gain ($88,000 – 7,000 = $81,000 x 20% = $16,200).

Example 3 Popeye and Olive Oyl are married and file a joint individual income tax return. Popeye earned $300,000 in wages as an employee for the Department of Defense in 2018. Olive Oyl owns 100% of the shares of Alessi, an S corporation that manufactures olive oil. Alessi generated $100,000 in net income from operations in 2018. Alessi paid Olive Oyl $150,000 in wages in 2018. Neither Popeye or Olive Oyl have any capital gains or losses. After allowable deductions not related to Alessi (i.e. personal itemized deductions) , Popeye and Olive Oyl’s total taxable income for 2018 is $300,000.

Popeye and Olive Oyl’s wages are not considered to be income from a trade or business for purposes of the QBI deduction. Because Alessi is an S corporation, its QBI is determined at the S corporation level. Alessi’s QBI is $100,000, the net amount of its qualified items of income, gain, deduction, and loss. The wages paid by Alessi to Olive Oyl are considered to be a qualified

item of deduction for purposes of determining Alessi’s QBI.

The QBI deduction with respect to Alessi’s QBI is then determined by Olive Oyl, Alessi’s sole shareholder, and is claimed on the joint return filed by Popeye and Olive Oyl. Their QBI deduction is equal to $20,000, the lesser of 20% of Olive Oyl’s QBI from the business ($100,000 x 20% = $20,000) or 20% of Popeye and Olive Oyl’s total taxable income for the year ($300,000 x 20% = $60,000).

Income within threshold examples

These limitations are phased in for joint filers with taxable income between $315,000 and $415,000, and all other taxpayers with taxable income between $157,500 and $207,500.

Example 4 Bonnie and Clyde are married and file a joint individual income tax return. Bonnie is a shareholder in Public Enemy, an entity taxed as an S corporation for Federal income tax

purposes that conducts a single trade or business (freight operations). Public Enemy holds no qualified property.

Bonnie’s share of Public Enemy’s QBI is $300,000 in 2018. Bonnie’s share of the W-2 wages from Public Enemy in 2018 is $40,000. Clyde earns wage income from employment by an unrelated company. After allowable deductions unrelated to Public Enemy, Bonnie and Clyde’s taxable income for 2018 is $375,000. Bonnie and Clyde are within the phase-in range because their taxable income exceeds the applicable threshold amount, $315,000, but does not exceed the threshold, or $415,000. Consequently, the QBI component of Bonnie and Clyde’s QBI deduction may be limited by the W-2 wage and UBIA limitations but the limitations will be phased in.

The UBIA of qualified property limitation amount is zero because Public Enemy does not hold

qualified property. Bonnie and Clyde must apply the W-2 wage limitation by first determining

20% of Bonnie’s share of Public Enemy’s QBI. This amount equals $60,000 ($300,000 x 20%). Next, Bonnie and Clyde must determine 50% of Bonnie’s share of Public Enemy ’s W-2 wages. This amount is $20,000 ($40,000 x 50%).

Because 50% of Bonnie’s share of Public Enemy’s W-2 wages ($20,000) is less than 20% of her share of Public Enemy’s QBI ($60,000), Bonnie and Clyde must determine the QBI component of deduction by reducing 20% of Bonnie’s share of Public Enemy’s QBI by the reduction amount.

Bonnie and Clyde are 60% through the phase-in range (that is, their taxable income of $375,000 exceeds the threshold amount by $60,000 and their phase-in range is $100,000). Bonnie and Clyde must determine the excess amount, which is the excess of 20% of Bonnie’s share of Public Enemy’s QBI, or $60,000, over 50% of Bonnie’s share of Public Enemy’s W-2 wages, or $20,000. Thus, the excess amount is $40,000. The reduction amount is equal to 60% of the excess amount, or $24,000 ($40,000 x 60%).

Thus, the QBI component of Bonnie and Clyde’s deduction is equal to $36,000, 20% of Bonnie’s $300,000 share Public Enemy’s QBI (that is, $60,000), reduced by $24,000. Bonnie and Clyde’s QBI deduction is equal to the lesser of (i) 20% of the QBI from the business as limited ($36,000) or (ii) 20% of Bonnie and Clyde’s taxable income ($375,000 x 20% = $75,000). Therefore, Bonnie and Clyde’s deduction is $36,000 for 2018.

Example 5 Assume the same facts as in Example 4, except that Public Enemy was engaged in a SSTB (consulting). Because Bonnie and Clyde are within the phase-in range, Bonnie must reduce the QBI and W-2 wages allocable to Bonnie from Public Enemy to the applicable percentage of those items as a proportion to the phase out range. Furthermore, she must apply a reduction amount to the calculation.

The applicable percentage equals 100% minus the percentage obtained by dividing (a) the pre-QBI deduction taxable income of the taxpayer in excess of the applicable threshold amount by (b) $100,000 for joint-return filers or $50,000 for other filers. Reduction amount means, the excess amount multiplied by the applicable percentage. It is calculated as 20 percent of QBI over the greater of 50 percent of W-2 wages or the sum of 25 percent of W-2 wages plus 2.5 percent of the UBIA of qualified property.

For Bonnie and Clyde’s applicable percentage, their taxable income ($375,000) exceeds their threshold amount ($315,000) by $60,000. A ratio of 60% (i.e. $60,000/$100,000) is what is used to find their applicable percentage of 40% (i.e. 100% – 60% = 40%). Accordingly, in computing the QBI deduction, the couple would only be allowed to take into account 40% of the QBI, W-2 wages, and qualified property with respect to the trade or business.

Thus Bonnie’s QBI is “adjusted” to $120,000 ($300,000 x 40%) and her share of W-2 wages is “adjusted” to $16,000 ($40,000 x 40%). These “adjusted” numbers must then be used to determine how Bonnie’s QBI deduction is limited. The deduction will be limited to the lesser of:

- (i) 20% of Bonnie’s share of Public Enemy’s QBI or

- (ii) the greater of the W-2 wage or UBIA of qualified property limitations.

- Twenty percent of Bonnie’s share of QBI of $120,000 is $24,000.

- The W-2 wage limitation equals 50% of Bonnie’s share of Public Enemy’s wages ($16,000 x 50%) or $8,000.

- The UBIA of qualified property limitation equals $0

To calculate the reduction amount Bonnie and Clyde must first determine the excess amount. This is calculated as the excess of 20% of Bonnie’s share of Public Enemy’s QBI, as adjusted ($24,000), over 50% of Bonnie’s share of Public Enemy’s W-2 wages, as adjusted ($8,000). Thus, the excess amount is $16,000. The reduction amount is equal to 60% of the excess amount or $9,600. Thus, the QBI component of Bonnie and Clyde’s QBI deduction is equal to $14,400 ($24,000 – $9,600).

As Bonnie and Clyde’s QBI deduction is equal to the lesser of (i) 20% of the QBI from the business as limited ($14,400) or 20% of Bonnie’s and Clyde’s taxable income ($375,000 x 20% = $75,000), their QBI deduction is $14,400 for 2018.

Income above threshold examples

Example 6 Ernie, an unmarried individual, is a 30% owner of Bert LLC, which is classified as a partnership for Federal income tax purposes. In 2018, Bert LLC has a single trade or business (landscaping) and reported QBI of $3,000,000. Bert LLC paid total W-2 wages of $1,000,000, and its total UBIA of qualified property is $100,000. Ernie is allocated 30% of all items of the partnership. For the 2018 taxable year, Ernie reports $900,000 of QBI ($3,000,000 x 30%) from Bert LLC . After allowable deductions unrelated to Bert LLC (i.e. personal itemized deductions), Ernie’s taxable income is $880,000.

Because Ernie’s taxable income is above the threshold amount, the QBI component of Ernie’s QBI deduction will be limited to the lesser of:

- (i) 20% of Ernie’s share of Bert LLC’s QBI or

- (ii) the greater of the W-2 wage or UBIA of qualified property limitations.

So while it might not be clear, there are three calculations related to the two bullets above:

- Twenty percent of Ernie’s share of QBI of $900,000 is $180,000.

- The W-2 wage limitation equals 50% of Ernie’s share of Bert LLC’s wages ($1,000,000 x 30% = $300,000 x 50%) or $150,000.

- The UBIA of qualified property limitation equals $75,750, the sum of:

- (i) 25% of Ernie’s share of Bert LLC’s wages ($1,000,000 x 30% = $300,000 x 25%) or $75,000 plus

- (ii) 2.5% of Ernie’s share of UBIA of qualified property ($100,000 x 30% = $30,000 x 2.5%) or $750.

For items 2 and 3 above, the greater of the limitation amounts ($150,000 and $75,750) is $150,000.

The QBI component of Ernie’s QBI deduction is thus limited to $150,000, the lesser of (i) 20% of QBI ($180,000) and (ii) the greater of the limitations amounts ($150,000). Ernie’s QBI deduction is equal to the lesser of (i) 20% of the QBI from the business as limited ($150,000) or (ii) 20% of Ernie’s taxable income ($880,000 x 20% = $176,000). Therefore, Ernie’s QBI deduction is $150,000 for 2018.

Ready to get help? As you can tell, the computations involved in taking the deduction get more complicated depending on the taxpayers income. If you don’t want to go through the mechanics of calculating your QBID and ensuring it is correct, why not let a professional do the work? Feel free to give us a call or drop us an email and we’d be happy to assist you ensure that everything is done correctly. Plus, you won’t have to spend the time doing it!